When you’re considering a graduate plus loan program, what are the terms? In this article, we’ll give you an overview of the different types of graduate plus loans and their terms. After reading this article, you should have a better understanding of what to look for when deciding which program is right for you.

What is a grad plus loan?

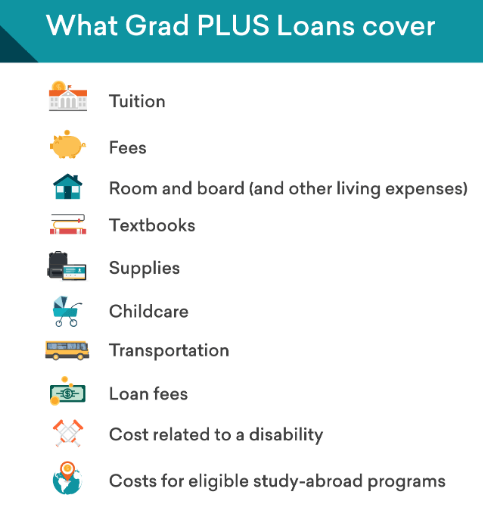

what is a grad plus loan? Grad PLUS Loans are federally-backed, private loans that graduate students can borrow to cover the costs of attendance after completing a qualifying program. The loan is available in two forms: Direct and Consolidation.

Direct offers borrowers a fixed interest rate and no origination fees. This type of loan is best for those who want to borrow quickly and have little to no credit history. Consolidation allows borrowers to combine multiple Direct Grad PLUS Loans into one large loan with a fixed interest rate and no origination fees.

What are the benefits of getting a grad plus loan?

A grad plus loan is a type of student loan that combines federal loans with private loans. This way, students can get the best possible terms and conditions for their borrowing. The benefits of getting a4r include:

– Better terms: Private lenders usually offer borrowers better terms than the government lenders, so you’re likely to pay less in total.

– Increased flexibility: A allows you to use your loans more flexibly, which can make your repayment process easier.

– Reduced interest rates: You may be able to get reductions on your interest rates if you have a good credit history.

How much does a grad plus loan cost?

Grad PLUS Loan programs are designed to help students who have completed a bachelor’s degree and are seeking to further their education by taking on additional debt. The terms of vary depending on the lender, but typically the loan amount is based on your undergraduate debt load and your anticipated graduate school expenses.

There are several factors to consider when determining the cost. First, you will need to know what your undergraduate indebtedness is as this will determine how much of a down payment you will need for the loan. Second, you will need to estimate what your total expected graduate school expenses will be. This includes tuition, room and board, and other associated costs such as books, supplies, and transportation. Finally, you will need to calculate your monthly repayment obligations using an interest rate that is applicable to your situation.

When is the best time to get a grad plus loan?

There are a few key factors to consider when determining when is the best time to get a grad plus loan. The interest rates and available borrowing capacity will vary depending on your individual situation, but generally speaking, getting a loan before you graduate can be advantageous because the interest rate is typically lower than after you graduate. Additionally, your borrowing capacity may be greater if you have good credit history and don’t have any outstanding debt. You should also keep in mind that the terms of a can vary significantly based on lender. Some offer fixed-rate loans with no early repayment penalties, while others allow for variable interest rates that could increase over time

Conclusion

Grad PLUS loans are a great way to finance your graduate degree. They come with flexible terms, low interest rates, and the ability to borrow up to $120,000 total. Plus, you can take advantage of federal and state financial aid opportunities that are available through your school. If you’re interested in taking out a grad PLUS loan, be sure to speak with your lender about the terms and conditions of the loan before making an application.